Learn how to use AI in accounting to automate routine tasks, improve accuracy, accelerate reporting, and streamline financial workflows.

TL;DR

- The capacity bottleneck in accounting firms is rarely complex judgment work. It is the manual movement of data across disconnected portals, spreadsheets, and ERP systems that eats up billable hours.

- Native ERP features only function within their own databases. True agentic systems execute cross-platform workflows by navigating external portals and extracting mixed-format documents as a human operator would.

- Modern extraction models read contextually instead of relying on rigid, per-vendor templates. This means scanned PDFs, messy spreadsheets, and client emails can all pass through a single ingestion pipeline.

- Deploying models on messy upstream data only multiplies errors faster than a human could. Standardization of inputs across formats and sources is a hard prerequisite for any processing pipeline.

- You cannot delegate CPA liability to software. Models exist to draft entries, categorize transactions based on historical patterns, and flag anomalies, but human review remains a non-negotiable compliance requirement.

- Start with a single, highly repeatable workflow rather than a massive overhaul. Measure the manual hours it takes beforehand, deploy the system, and confirm the error rates drop before expanding to other clients.

Why Traditional Accounting Workflows Struggle to Scale

Most finance teams reach an inflection point quietly. Client count grows; headcount doesn't. The work expands to fill whatever hours staff have left, and the only lever available is to extend the workday. According to Gartner's 2025 AI in Finance Survey of 183 CFOs and senior finance leaders, 59% of finance functions are already using AI in some capacity, up from 37% in 2023. The gap between that 59% and the rest isn't knowledge; it's operational urgency.

The AI market in accounting reached $7.52 billion in 2025 and is projected to grow to $50.29 billion by 2030, expanding at a 46.2% CAGR, according to Mordor Intelligence. That growth rate reflects something real: accounting workflows have enough volume, enough repetition, and enough structure to make automation genuinely viable at scale, not just in proof-of-concept environments.

Gartner also predicts that finance organizations using cloud ERP applications with embedded AI will achieve a 30% faster financial close by 2028, as agentic AI, machine learning, and process orchestration take over reconciliation and collections work currently performed by human staff.

This article covers where AI fits in an accounting workflow step by step, how to distinguish between AI-assisted tools and agents that run full workflows, how to deploy without replacing your existing stack, and what goes wrong when implementation skips the right steps.

The Repeatable Work That Eats CPA Capacity

The bottleneck in most CPA firms isn't complex judgment work. It's the volume of identical, low-variance tasks that repeat every engagement, every month, every client.

A typical client engagement involves logging into multiple bank portals individually, downloading statements in whatever format each portal exports, renaming and reformatting files to match internal templates, copying data into Excel, and then re-entering it into QuickBooks. Adopt AI's accounting agents documentation describes this pattern explicitly: CPAs navigating 15 separate portals, running Python scripts to rename files, extracting to Excel, then re-entering into QuickBooks. The work isn't intellectually demanding. It's time-intensive and scales linearly with client count, meaning every new client adds proportionally to the manual load.

The output of one typical engagement that should take two hours routinely takes 20, not because the accounting is complex, but because the data collection and formatting work sits between systems that don't talk to each other.

Why Existing Software Hasn't Closed the Gap Yet

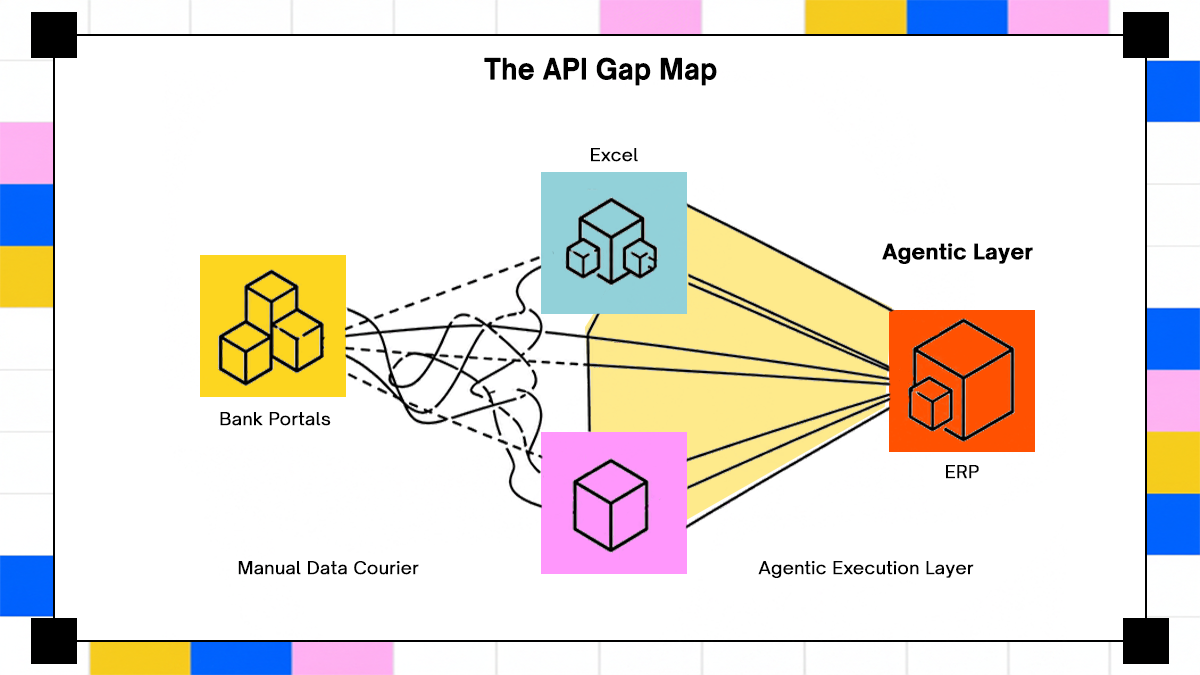

ERPs and close management platforms automate within their own data models. QuickBooks automates within QuickBooks. NetSuite automates within NetSuite. The work that falls between systems, like logging into a bank portal, downloading a scanned statement, and getting the data into the ERP, stays manual because no standard API connects those surfaces.

Nearly 46% of small and mid-sized accounting firms report a lack of internal AI expertise, which significantly slows adoption despite growing interest in automation. The result is a split reality: firms that are well-tooled on paper but manually intensive in practice, because the automation their software provides stops at the edge of its own ecosystem.

The integration problem is the actual problem. Most accounting firms already have QuickBooks, Excel, and some combination of bank feeds and payroll exports. What they don't have is anything that bridges those systems without a human acting as the connector.

What's Changed in the Last 18 Months That Makes Automation Viable Now

Three specific shifts have moved this from theoretical to deployable.

Natural language models now extract key fields from invoices, contracts, and receipts at accuracy levels exceeding 95%, effectively eliminating the keyboard bottlenecks that have long stalled accounts-payable teams. Earlier OCR required per-vendor template configuration; when a vendor changed their invoice layout, accuracy dropped and the document was routed to manual review. Current document intelligence reads content contextually, understanding what a field means rather than where it sits on the page.

Agentic platforms now complete workflows end-to-end rather than assisting with individual steps. An agent can receive a goal, plan the steps, log into external systems, handle exceptions, and produce a completed output with an audit trail, without requiring a developer to script each interaction. And no-code interfaces have made it possible for accounting staff to configure and run these agents without engineering support, removing the dependency on IT resources that historically delayed or killed automation projects.

Where AI Actually Fits in an Accounting Workflow, Step by Step

Understanding where AI operates well across an accounting workflow requires mapping the workflow first, then identifying which stages involve structured repetition versus judgment calls. The breakdown below follows the work chronologically, from document intake to reconciled ledger, and is specific about what gets handed off and what doesn't.

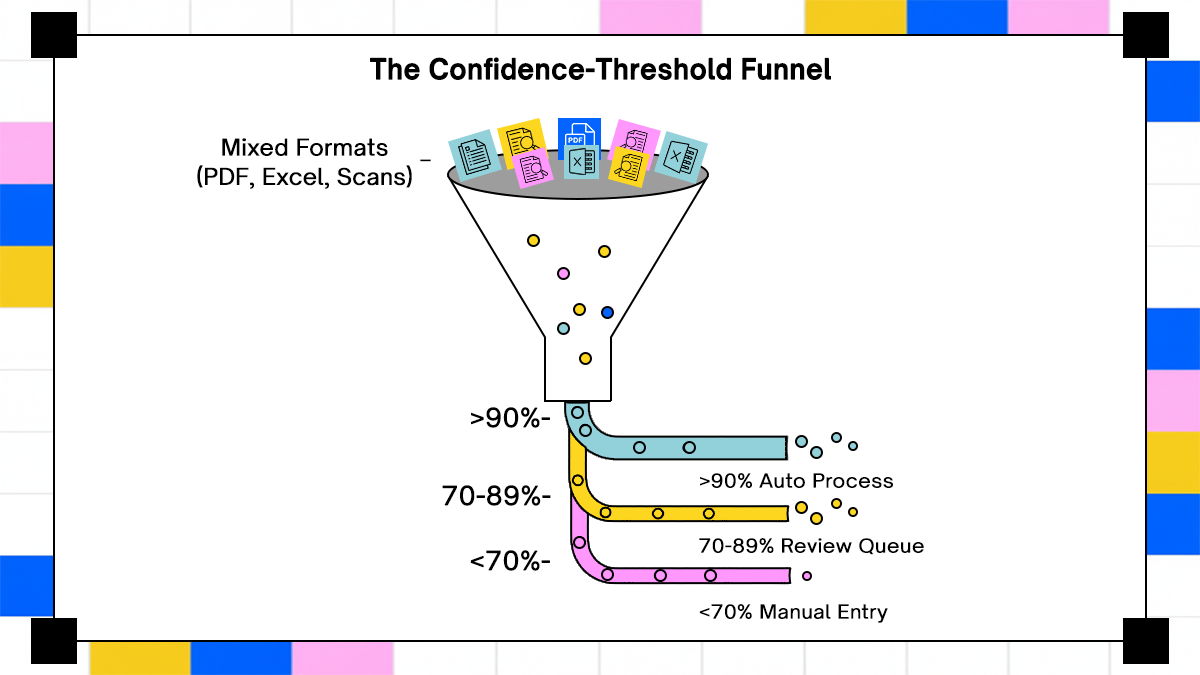

Data Ingestion and Document Extraction Across Mixed Formats

Document intake is where the format problem lives. Clients send clean Excel payroll exports, scanned PDFs from their bank, physical mail that gets digitized, and call transcripts from vendor negotiations. A single client engagement can involve four or five different document types arriving through different channels.

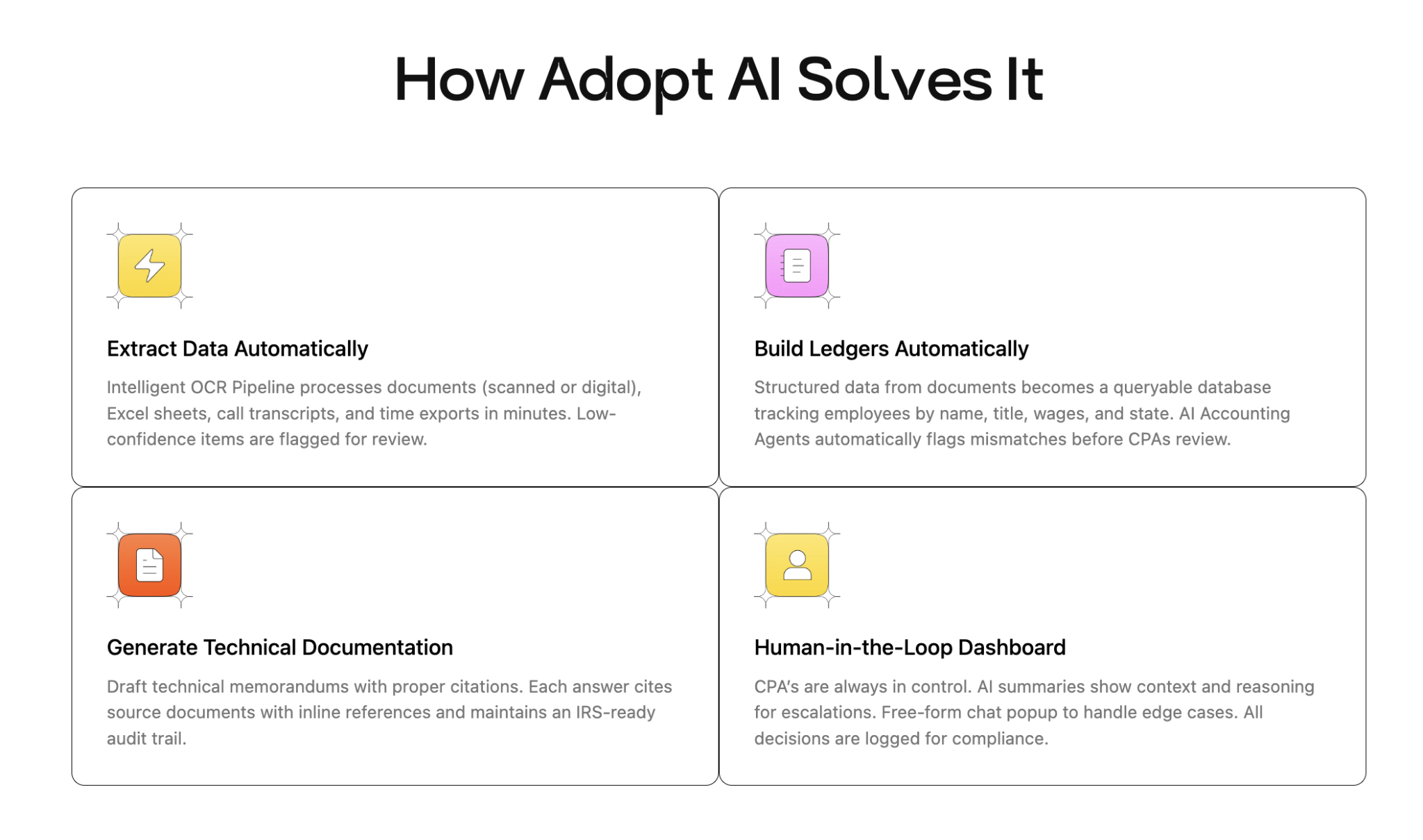

An OCR pipeline operating in production handles all of these formats without requiring separate templates for each source. Adopt AI's accounting agents workflow processes scanned and digital documents, Excel sheets, call transcripts, and time exports within the same pipeline. Items where the model's confidence falls below a set threshold get flagged for human review rather than passed through silently.

The threshold setting is where firms make a real decision. A tighter confidence threshold produces cleaner output but more review items. A looser threshold processes more automatically but raises the risk of extraction errors reaching downstream steps. Most firms run a tighter threshold initially and loosen it as they validate accuracy over several months of production data. The tradeoff isn't fixed; it's calibrated against the firm's error tolerance and client profile.

Ledger Population, Transaction Categorization, and Anomaly Detection

Once documents are extracted, structured data needs to populate queryable records and the general ledger. Adopt AI's system builds a database tracking employees by name, title, wages, and state from payroll documents, and populates ledger entries from bank statement data. The categorization step uses historical coding patterns from prior periods rather than guessing at category assignments based on the transaction description alone.

The distinction between supervised and unsupervised categorization matters in CPA work. Supervised categorization applies pre-approved formulas and coding rules validated by a CPA. Unsupervised categorization, where the model makes independent judgments about account mapping, introduces an unacceptable risk in client-facing engagements where the CPA carries professional liability. Adopt AI's documentation specifically notes that complex queries are routed through an RAG framework and that pre-approved formulas avoid unsupervised AI math.

Anomaly detection at this stage catches problems that don't surface until close under manual workflows: duplicate entries across document sources, amounts that don't reconcile between bank data and payroll, and transactions that pattern-match to prior-period exceptions. Catching them here, before a human reviews the ledger, compresses the correction cycle from days to hours.

Financial Close Support, Reconciliation, and Exception Handling

The monthly close is when accumulated data quality issues from prior steps either surface cleanly or require hours of manual correction. AI operates on two fronts here.

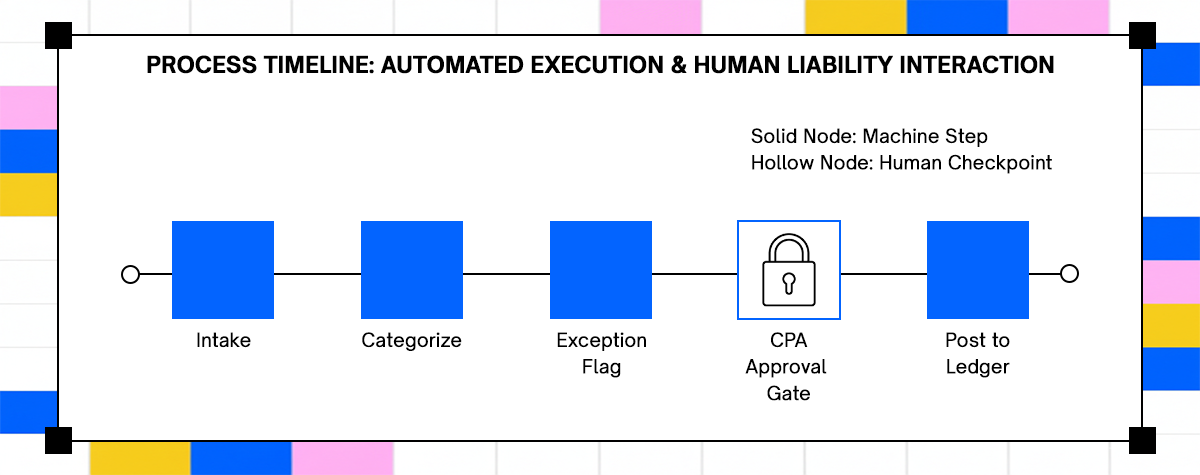

First, automated reconciliation flags mismatches in bank statements, ceding statements, and reserves before CPAs begin their review. Items that reconcile automatically don't require any CPA time. Items that flag are presented with the AI's reasoning for the escalation, so the CPA doesn't have to start from scratch to understand why a mismatch was detected.

Second, exception handling uses a human-in-the-loop dashboard where CPAs can review flagged items, approve or override AI suggestions, and use free-form chat for edge cases that don't fit standard exception patterns. Every decision is logged for compliance, maintaining an audit trail that covers both what the agent processed and what the CPA reviewed.

CPA firms cannot delegate final judgment to an automated system. Professional liability doesn't transfer with the task. The human-in-the-loop gate isn't a workaround for AI limitations; it's structurally necessary given how CPA liability works.

AI Agents vs. AI-Assisted Tools: What the Distinction Means for Accounting Teams

The difference between embedded AI features and agentic systems isn't a matter of degree; it's a structural difference in what each can actually do. Teams conflating the two end up either disappointed by the ceiling on embedded tools or deploying agents in contexts where they're not the right fit.

What Embedded AI in Accounting Platforms Does

Embedded AI in platforms like NetSuite, QuickBooks, or close management software operates within the platform's own data model. It can draft variance explanations from GL data, suggest journal entries, match bank transactions, and surface anomalies within the data the platform already holds.

Numeric's flux AI writer is a clear example: it generates variance explanations from GL data automatically, within Numeric's platform, for Numeric customers. It doesn't pull data from external portals, log into bank systems, or handle document formats that haven't been imported into Numeric's data model. That's the ceiling. It's a high-quality, well-scoped tool for one element of the month-end workflow.

The gap that embedded AI doesn't close is the work that happens outside the platform's ecosystem: unstructured documents arriving from external sources, portal logins with no API, and cross-system data transfer. That gap is where most of the manual hours live.

When Agentic AI Takes Over the Full Process

An accounting agent receives a goal ("complete the bookkeeping for client X this month"), breaks it into steps, executes across the relevant systems, handles exceptions per defined rules, and produces a completed output. The agent logs into bank portals, downloads statements, extracts data from mixed-format documents, populates the ledger, flags anomalies, and routes exceptions to a human review queue, without requiring manual steps between each stage.

The mechanism that makes this work across systems with no public API is Application Use: the agent navigates software interfaces the way a human does, reading the screen, clicking through workflows, and extracting data from surfaces that have no programmatic access. Adopt AI describes this explicitly as operating across internal tools, external portals, and legacy systems without requiring systems to be rebuilt or replaced.

Agentic AI is appropriate when the workflow is well-defined, repeatable, and stable enough that the steps don't change unpredictably between runs. It's not appropriate for judgment-heavy work or for workflows where the inputs are too variable to process reliably.

The Control and Compliance Architecture That Makes Agents Safe for CPA Work

Before deploying agents on client financial data, CPA firms need answers to four questions: Is every agent action logged and auditable? Can access be restricted by role? Can the system run on-premises for clients whose data can't leave their environment? Are human approval gates enforced at the right checkpoints?

Adopt AI's documented capabilities address each: comprehensive audit logging of every agent run, role-based access control (RBAC) for restricting access by job function, on-premises and hybrid deployment options for InfoSec-constrained environments, and human-in-the-loop dashboards where CPAs approve exceptions before they post.

The audit trail isn't optional for accounting work. IRS-ready documentation, client reporting, and internal compliance all depend on knowing exactly what the system processed, when, and with what outcome. An agent that processes without logging creates a liability exposure that no efficiency gain can justify.

AI Accounting Platforms vs. Agentic Accounting Systems

The accounting AI market now includes several categories of tools, each solving a different part of the workflow. Understanding these categories helps accounting teams evaluate where a platform fits and what level of automation it can realistically provide.

The first category is embedded AI within existing accounting platforms. Solutions integrated into products such as ERP systems, close management tools, and accounting software help automate tasks within their respective ecosystems. Common capabilities include transaction matching, variance analysis, reconciliation support, anomaly detection, and draft journal entry generation. These tools improve productivity but generally operate only on data already available inside the platform.

The second category is accounting automation platforms built around a new operating environment. These systems often require firms to adopt new workflows, migrate processes to the vendor's platform, and retrain teams to work differently. While they can automate substantial portions of accounting work, implementation frequently involves platform migration and process redesign.

The third category is agentic accounting systems. Rather than replacing existing software, these platforms operate across the tools firms already use. Agents execute workflows spanning ERP systems, bank portals, spreadsheets, document repositories, government portals, and legacy applications. The objective is not simply to assist accountants on one platform, but to automate the movement of work across multiple systems while preserving human review and audit controls.

This distinction becomes important because most accounting bottlenecks occur between systems rather than inside them. Downloading statements, collecting client data, moving information between portals, reconciling records across platforms, and preparing filings often require accountants to act as the integration layer between disconnected applications. Traditional automation improves individual tasks. Agentic systems attempt to automate the workflow that connects them.

How Adopt AI Differs

Many accounting automation vendors focus primarily on assisting with work inside a dedicated platform. Adopt AI takes a different approach by adding an agent layer on top of an organization's existing accounting stack rather than requiring firms to replace their current tools. According to Adopt AI's platform documentation, agents can operate across ERP systems, external portals, spreadsheets, workpapers, and government filing systems without requiring a platform migration. You can check this for a detailed comparison of this approach against traditional accounting automation platforms.

Another distinction is support for what Adopt AI calls the "last mile" of accounting workflows. Beyond document extraction and transaction processing, agents can retrieve information from portals that do not expose APIs, complete workflow steps across multiple systems, and participate in filing processes that traditionally require manual intervention.

For firms with strict governance requirements, Adopt AI also supports deployment models in which workflow history, audit trails, and operational data remain within the organization's infrastructure via on-premises or private cloud deployments. This differs from cloud-only approaches that require firms to move operational data into a vendor-managed environment.

Implementing AI in Accounting Without Rebuilding Your Tech Stack

Most AI implementation guidance assumes you're building from scratch. CPA firms aren't. They have QuickBooks Desktop, Excel templates that clients send payroll data in, bank portals that export in whatever format the bank chooses, and Slack for internal coordination. The deployment question isn't "what stack do we build?" but "what can we connect to what already exists?"

Mapping Your Highest-Friction Workflow Before Choosing a Tool

Before selecting a tool, map one complete client engagement from intake to trial balance and count every manual step. The specific question to answer for each step: is a human performing this task because it requires judgment, or because two systems don't connect automatically?

The steps where a human is acting as a data courier between disconnected systems are the deployment targets. In most CPA firm engagements, those steps cluster around bank portal downloads, file reformatting, and ERP re-entry. Pick the one workflow where the manual steps are most predictable and the data formats are most consistent. Deploy there, measure before and after, and expand only after confirming the first workflow performs reliably in production.

The sequencing principle matters: one workflow, measured, before any scope expansion. Teams that try to automate broadly before validating narrowly end up with unreliable automation across multiple workflows and no clean baseline to diagnose what's failing.

Connecting to Systems That Don't Have APIs

A large portion of accounting manual work happens in systems with no API: bank portals, client vendor platforms, state tax portals, and legacy ERP screens. Traditional RPA tools handle these through brittle UI scripting that breaks when the portal updates its layout, requiring manual fixes each time.

Agents operating via Application Use adapt to interface changes because they read the screen contextually rather than relying on fixed element coordinates or CSS selectors. When a bank portal updates its login flow or changes the button label on a statement download, the agent reads the updated interface and completes the task rather than failing and requiring a developer to update the script.

The practical difference for accounting teams is that agent-based connections to portal-only systems require less ongoing maintenance than RPA scripts and can handle format changes from the portal vendor without breaking downstream workflows.

Measuring ROI Before Scaling to Additional Clients

The metrics that justify expansion for CPA firms are specific: hours per client per engagement (before and after), error rate on reconciliations, close cycle length, and client volume handled per FTE.

Adopt AI's accounting agent deployment documents a 90% reduction in manual hours per client, from 20 hours to 1-2 hours per engagement, and a 2x increase in client capacity without proportional headcount growth. Those numbers are the target baseline for a first deployment measurement. If your first workflow doesn't produce comparable numbers, investigate before expanding scope; the issue is usually upstream data quality or a workflow that's less consistent than it appeared during scoping.

Build the before/after measurement before deploying, not after. You need a clean baseline that captures actual hours per client across a representative sample of engagements. Post-deployment comparisons against recollection aren't defensible in budget conversations.

Common Failure Modes When Accounting Teams Implement AI

Implementation guides tend to describe what works. What follows is what breaks, grounded in the patterns that surface in production accounting deployments.

Automating Downstream Before Fixing Upstream Data Quality

The most common deployment mistake is deploying AI on reconciliation or close workflows before the upstream data is consistent. If bank feeds export in different date formats across portals, if payroll exports vary by quarter, or if client Excel files arrive with inconsistent column structures, the extraction pipeline will produce unreliable output regardless of how good the AI model is.

AI propagates bad data faster than a human does, because it processes volume that a human wouldn't attempt manually. A human reviewing 200 transactions will notice something looks wrong partway through. An agent processing 2,000 transactions will complete the run, and the errors will surface at reconciliation with no easy way to trace which input caused which discrepancy.

Before deploying any automated pipeline, validate that the source data has been stable for at least 3 prior months. If it isn't, standardize the upstream format first. The automation layer should sit on top of clean inputs, not be expected to clean them.

Skipping the Human Review Gate and What It Costs

Some teams treat the human review checkpoint as optional overhead once the agent has been running reliably for a few months. Removing it creates three categories of risk.

Audit exposure comes first: if an agent posts journal entries without CPA review and an error surfaces during the audit, the firm has no documented human decision to point to. Second, correction costs. Errors caught before posting take minutes to fix. Errors caught post-close, after client reports have been generated, take hours and may require restatement. Third, client trust. A client whose accounts are materially misstated due to an unreviewed agent run is unlikely to remain a client.

The human review gate isn't a temporary concession to AI immaturity. It's the same control a CPA firm would apply to work done by a junior accountant: review before it leaves the firm. The agent's work product is a draft, not a final output.

Tool Selection Misfit: General-Purpose LLMs vs. Accounting-Specific Agents

General-purpose LLMs like ChatGPT or Claude are genuinely useful for CPA teams for specific task types: drafting client emails, summarizing accounting standards, generating policy memo first drafts, or answering technical GAAP questions quickly. Numeric's technical accounting AI, trained on GAAP guidance and Big 4 audit firm guidance, extends this for standard-specific questions.

What general-purpose LLMs can't do: maintain workflow state across multi-step processes, log into external systems, maintain an audit trail of actions, enforce RBAC, or handle structured exceptions with business rules. Using a general-purpose LLM to execute a bookkeeping workflow is like using a spreadsheet to manage a database: technically possible for small volumes, fundamentally wrong at scale.

The tool selection decision maps to the task type. General LLMs handle communication and research. Embedded AI handles within-platform assistance. Agentic platforms handle cross-system workflow execution. Mixing these up in either direction produces either over-engineered solutions for simple tasks or underpowered tools for complex ones.

Conclusion

Accounting teams that want to use AI effectively need to answer three questions before touching a vendor demo: which workflow has the most predictable manual steps, what does the upstream data quality look like for that workflow, and where human review must remain regardless of automation depth.

The article above covers where AI fits, step by step, across the accounting workflow; how embedded tools and agentic systems differ in capabilities and appropriate use; how to deploy against an existing tech stack without rebuilding it; and what common failure modes look like in production. Gartner's analysis puts it plainly: the biggest returns will come from managing finance technology as a portfolio, strengthening proven applications, accelerating high-value automation, and scaling AI where governance and integration are maturing, not from chasing isolated pilots. Start narrow, measure it, and build from there.

FAQs

1. Can AI Handle Accounting Tasks Without a Certified Accountant Reviewing the Output?

No, and it shouldn't. AI handles data extraction, categorization, ledger population, and anomaly flagging reliably at volume, but CPA firms carry professional liability for the accuracy of client financials. Every agent-processed output needs a human review checkpoint before posting. The agent's job is to reduce what the CPA needs to review manually, not to remove the review entirely.

2. What Types of Accounting Workflows Are Ready for Full Agent Automation Today?

Bank statement download and extraction, document ingestion across mixed formats, transaction categorization using historical patterns, reconciliation mismatch flagging, and ledger population from structured data are all in production at accounting firms today. Tax credit calculation (QRE aggregations), form population, and technical memo generation are also documented as agent-handled workflows. Judgment-heavy work, such as audit opinions, advisory work, and exception resolution, still requires a CPA.

3. How Does AI in Accounting Handle Unstructured or Scanned Financial Documents?

Modern document intelligence models read content contextually rather than matching against fixed templates. Items below the firm's configured confidence threshold automatically route to a human review queue. Scanned PDFs, digitized physical mail, and non-standard vendor formats all process through the same pipeline without requiring per-vendor template configuration.

4. What Are the Data Security Requirements for Deploying AI Agents Across Client Financial Data?

At minimum: comprehensive audit logging of every agent action, role-based access control restricting who can view or modify client data, and documented data residency controls. For firms whose clients prohibit financial data from leaving their own environment, on-premises deployment is the requirement. Adopt AI supports cloud, on-premises, and hybrid deployment specifically to clear InfoSec requirements without requiring a rebuild of the underlying workflow configuration.

.svg)

.svg)

Take three minutes to find out which side of that line you are on.

Browse Similar Articles

Find Your Agentic AI Readiness Score

Every enterprise thinks they are building toward Agentic AI. But only few actually are.

Take three minutes to find out which side of that line you are on.